Wall Street has experienced its largest two-day loss in history, with a combined $6.6 trillion wiped off the value of publicly traded companies on Thursday and Friday alone.

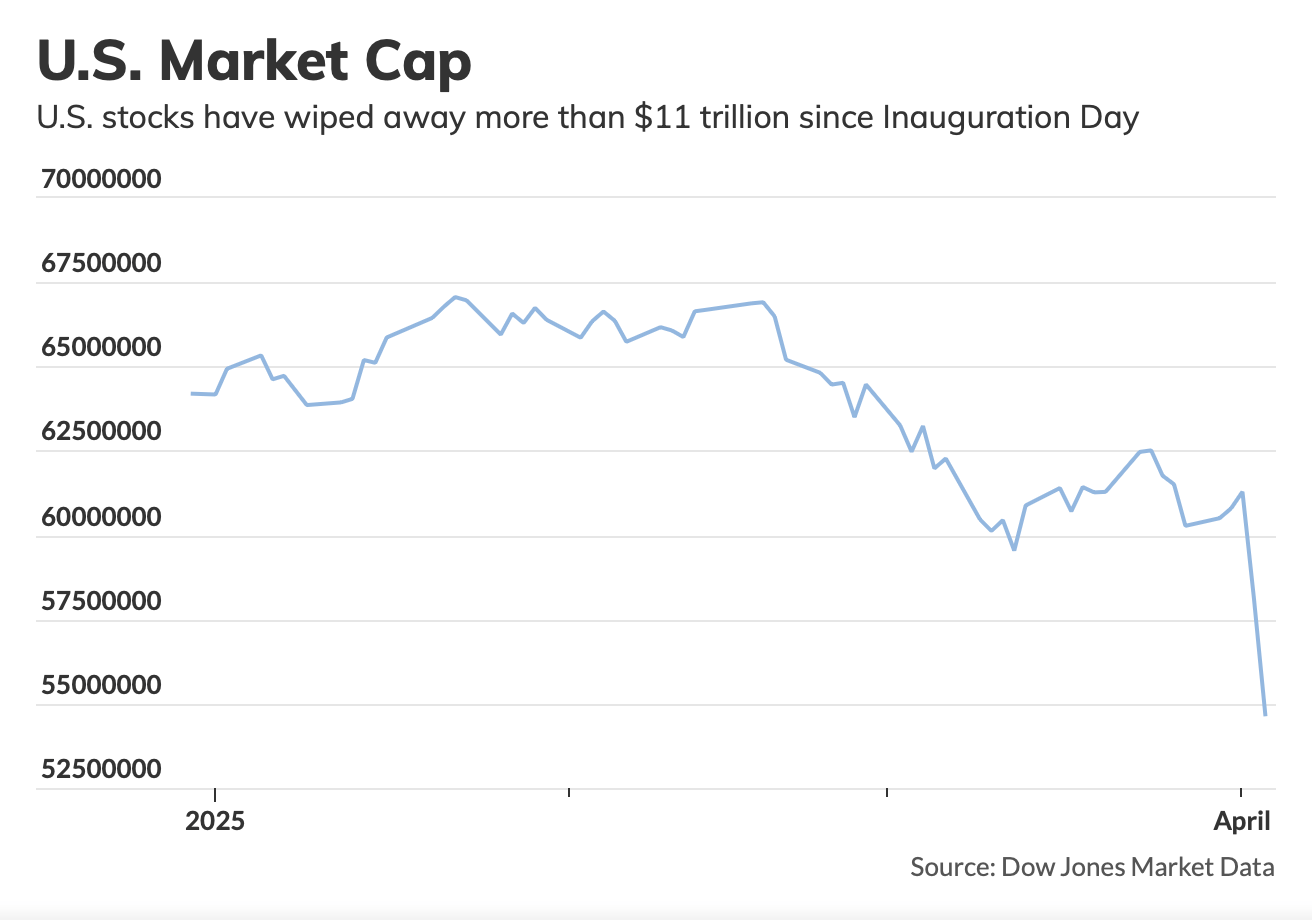

This development brings total losses since President Donald Trump’s second inauguration in January to approximately $11.1 trillion, according to data published by Dow Jones Market Data.

The downturn followed President Trump’s announcement on Wednesday of sweeping new tariffs, dubbed “liberation day” measures, which appear to have caught investors and analysts off guard. The scale and scope of the levies, which target a broad range of global imports, exceeded expectations and triggered a sharp market reaction.

The S&P 500 index closed Friday with a loss of 5.97%, while the Dow Jones Industrial Average (DJIA) dropped 5.50%. The Nasdaq Composite fell 5.82% on the day, bringing its total decline since peaking in February to over 22%, placing the tech-heavy index firmly in bear market territory. Similarly, the small-cap Russell 2000 index closed down 4.37% on Friday and is now more than 25% below its November 2024 high.

Overall, the DJIA has declined 11.9% since President Trump was sworn in for his second term on 20 January 2025. The S&P 500 has dropped 15.4% during the same period.

Despite a stronger-than-expected March employment report released Friday morning, concerns over the global economic impact of the new trade measures overshadowed positive labour market data. Jay Woods, chief market strategist at Freedom Capital Markets, stated in an email shared with MarketWatch that a continued escalation in trade tensions could have a substantial negative impact on the broader economy.

“If we are to punch back, you could have damaging effects to not only the tech sector, but the economy overall,” Woods said. “This could throw us into a recession and could end the bull market as we know it.”

President Trump, in an attempt to shore up confidence, posted on Truth Social that he had held a “productive” phone call with Vietnam’s leadership. Shares in Nike Inc., a company with significant manufacturing operations in Vietnam, rose 3% in response. However, this did little to mitigate the broader sell-off across equities.

Kathleen Brooks, research director at XTB, noted in a client briefing that financial markets are now looking to the administration for signs that the tariff package might be scaled back or that trade negotiations may resume. “Investors need a clear signal that the policy direction is not locked in,” she wrote.

The recent turmoil has drawn comparisons to previous presidential terms that began under market pressure. Losses on the S&P 500 have now surpassed those seen in the early days of George W. Bush’s first term in 2001, which were then driven by the collapse of the dot-com bubble.

According to research from Carson Group, equities typically perform more modestly during the first year of a new administration, particularly in the opening quarter. Performance tends to improve in the latter half of a presidential term, though such historical patterns offer little reassurance amid current volatility.

Friday’s performance marked the worst weekly showing for U.S. markets since March 2020, at the onset of the COVID-19 pandemic. The total value of U.S. equities, as tracked by Dow Jones Market Data, has declined from over $70 trillion in January to just under $59 trillion by the end of the week.

The scale of the losses is particularly significant given the relative stability in economic fundamentals prior to the tariff announcement. While recession risk was already a concern in some quarters, the shift in trade policy appears to have amplified fears of a sharp slowdown, particularly in sectors heavily reliant on global supply chains, such as technology and manufacturing.

Analysts have also pointed to the small-cap Russell 2000 index as a particular casualty of the current environment. FactSet data shows that the index, which tracks smaller U.S.-listed companies, has had its worst start to a presidential term on record.

Looking ahead, market participants are likely to remain focused on any signals from the White House indicating a shift in trade strategy or a softening of rhetoric. Absent such developments, volatility may persist, with investors weighing the risk of prolonged economic disruption against the possibility of renewed negotiations.

The extent to which the current sell-off reflects long-term structural concerns or a short-term reaction to policy uncertainty remains to be seen. However, the historic nature of the decline underscores the level of apprehension among investors and the sensitivity of financial markets to geopolitical and economic policy signals.

Read also:

Trump’s Trade Tariffs: A Dangerous Economic Gamble, Say European Lawmakers

{kind=link}